I was fortunate to have been invited to attend the first ever Female Founder's Conference hosted by Y-Combinator on March 1, 2014 at the Computer History Museum in Mountain View. Per Jessica Livingston, one of the founders of Y-combinator, this was the most oversubscribed event in the history of Y-combinator and they had to turn away several well qualified people who applied to attend. This, after the initial 150 people event at the YC office morphed to a 500 people event at the Computer History Museum!

Some aspects really stood out for me -

1. The commonality in our concerns and experience was striking, across different start-ups, stages and verticals, with gender being the only common factor.

Take for instance Jessica's experience putting together this conference. This was her brainchild, and she invested the time, effort, and energy into realizing her vision. Guess what Inc. magazine reported? This:

There was a collective groan from the audience when she shared this, and many heads were nodding in understanding. It left me wondering if there was any woman in the room who hadn't experienced this - work hard and accomplish something, but have the credit handed to a man, no matter how tangential or coincidental his involvement with the task.

2. One of the speakers asked for a show of hands from the audience to learn about audience backgrounds. A good 50+% of the all-women audience raised their hands when asked how many were engineers and programmers. That was plain awesome! Never in my life have I been surrounded by so many fellow women engineers.

I was hearing snatches of conversations about OS's, actuators, drivers, robots, APIs, REST interfaces and micro-controllers. It gave me such a kick, especially considering the stereotypes about how women only talk about clothes/fashion/babies/cute kittens and the like. There were fashionable women alright, but ambitious and brilliant geeks too and the conference was a testament to the fact that brains and beauty happily coexist with lovely, non-soap opera personalities.

3. The one thing that was a turn-off was the handful of founders who were trying to recruit the techies to work for their start-ups. This was a female founders conference. It was plain disrespectful to try and recruit someone at the conference. The attendees were there because they aspire to be founders. If you want to recruit engineers of any gender, go to Pycon or Ladies who code or one of the numerous other tech. events and meetups to find them. It's so not cool to ask people to give up on their aspirations and work for you, so you can further yours.

4. There were moms with babies in the audience, and there were moms who were successful founders on the stage! Jessica shared a photo of her working with her son in a bouncer on the table, next to the computer monitor. That brought a smile to my face. Reminded me of the hours I have logged thumb typing on the phone writing up a product spec while putting my little one to sleep, wearing the baby in an Ergo and taking conference calls walking around to keep her calm, and trying to work on the laptop with one hand while the other hand was occupied.

I tweeted the event live. Here are the relevant tweets from the event, with the oldest tweet starting at the bottom:

- Retweeted by Shuba S."I had a hot tub in my office... you don't want that!" What a great story @JessicaMah! @InDinero is going to kick ass #femalefounders

- @JessicaMah you were awesome! Love your unapologetic confidence :) #femalefounders pic.twitter.com/B3U4AO2OAx

- Inspiring talk by @JessicaMah. Brutally honest abt past mistakes and now unapologetically confident.Cheering her all the way!#femalefounders

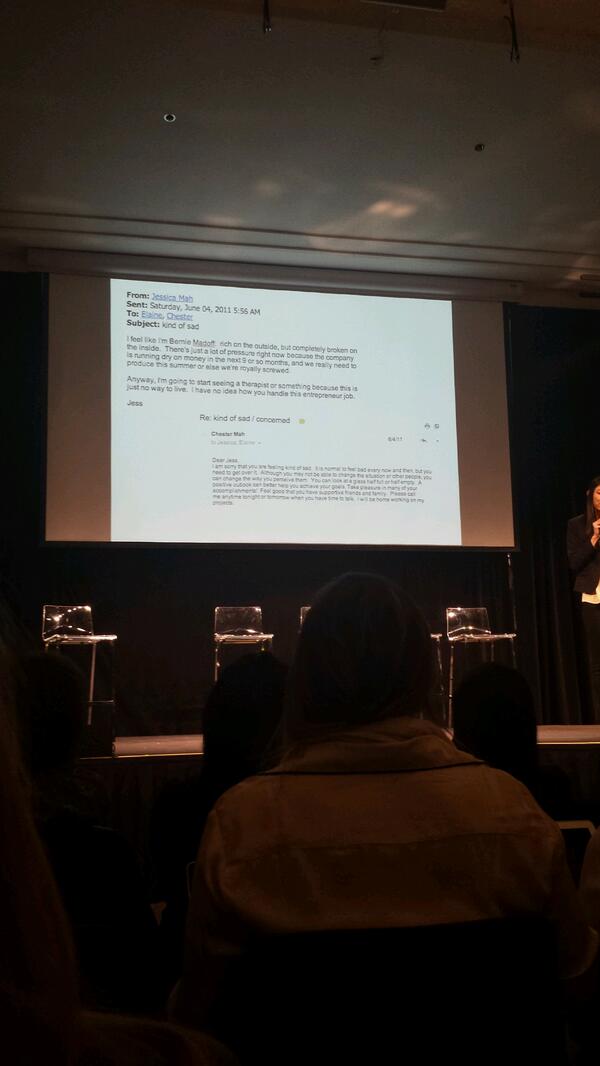

- Retweeted by Shuba S.It is normal to feel bad every now and then, but you need to get over it - @indinero founder @ycombinator #femalefounders

- @sgblank you just got a shout out on stage from Jessica "don't be afraid to pivot!" #femalefounders

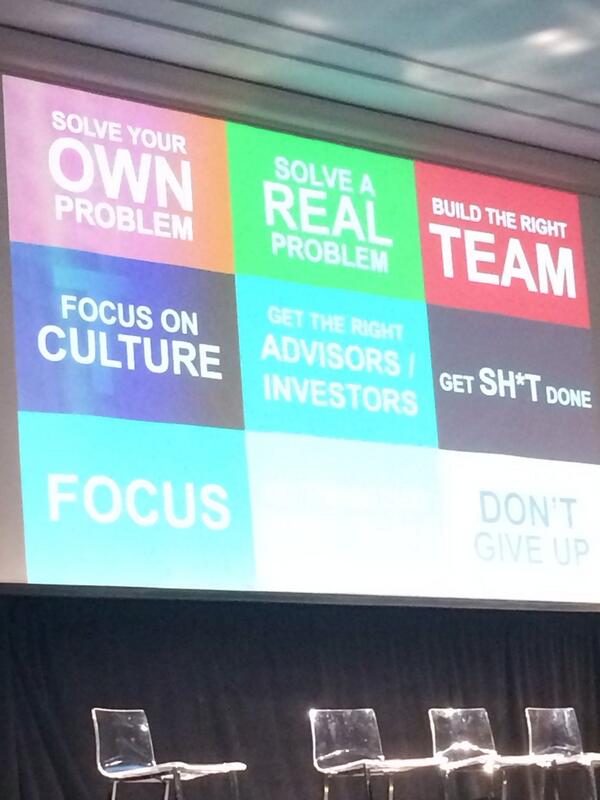

- Retweeted by Shuba S.Loved @elizabethiorns' talk at #femalefounders @ycombinator. Build the right team, Get shit done, Do things that don't scale, Don't give up.

- Great talk from Dr.Iorns! The summary in a slide. pic.twitter.com/yTduwiELAC

- "Do things that don't scale; it will teach you.", "focus on first 1000 users", some gems from Dr.Iorns of @ScienceExchange #femalefounders

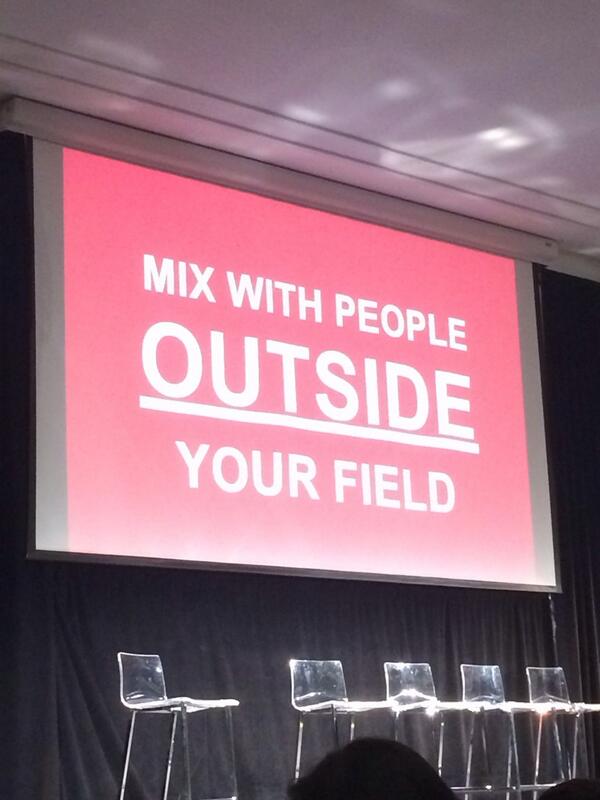

- Excellent advice, esp. for those of us who live in the Valley and drink the kool-aid #femalefounders pic.twitter.com/7mMUB5bd31

- Retweeted by Shuba S.RT @katygardiner: "Ambition is gender-neutral." Amazing quote from this fundraising panel #FemaleFounders

- Parting advice:be selective abt investors, don't jump through hoops - eg: add new slide bcos investor said so, ok to ignore #femalefounders

- @vayable Jamie's mom is a very wise woman. Named her daughter with a gender neutral name so no door is shut bcos she's a girl#femalefounders

- Retweeted by Shuba S.Avoid having to centralize your company HQ in 1 place by starting w/ 2 equally important, geographically separate locations. #femalefounders

- Retweeted by Shuba S.Crowd at the YC #femalefounders conf - look at all these people to be FUNDED! Hey Sequoia, you've got… http://instagram.com/p/lBWPskLhcb/

- Fundraising panel in progress. Interesting insight:ask the investors qns. Ask what value can you add to my company besides $ #femalefounders

- @vlgreen sitting in the front, near the door. Hope to bump into you this eve

- Diane hired the guy who came in to do her yard work to do QA @VMware.He turned out a rock star.Attitude matters > background #femalefounders

- Nobody is indispensable. Never let anyone hold you over a barrel. - Diane Greene (VMware) #femalefounders

- @vlgreen where are you? Sloanies represent!

- Great advice from @kmin don't believe the hype! #femalefounders

- Retweeted by Shuba S.“We got rejected by 11 incubators before getting into @ycombinator” @kmin founder @dailymuse #femalefounders pic.twitter.com/ZMSjAlL2T8

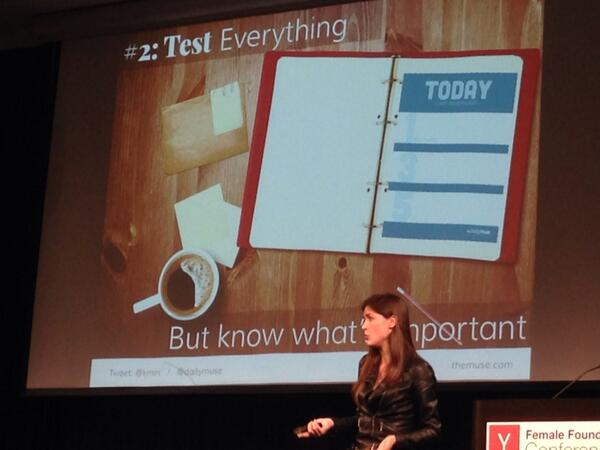

- Retweeted by Shuba S.@kmin great advice on testing everything but focusing on knowing what's important #FemaleFounders pic.twitter.com/pRLNAVtQEG

- @kmin user acq tips 1. Seek out like-minded groups 2. Ask for word of mouth and make it easy 3. Become your own PR machine #femalefounders

- @kmin advice: 1. start somewhere 2. Test everything 3. Create velocity #femalefounders

- Retweeted by Shuba S.Idea that resonates: start up as an "evolution from suck to suck-less" from @kmin at The Muse #femalefounders

- @kmin on stage now. Wanted to be Zorro as a kid and then in the CIA? We must be soul sisters :) #femalefounders

- Retweeted by Shuba S.based on eyeballing a handraise poll of the audience at #femalefounders conf, looks like 50+% of women here are engineers. pretty cool!

- Hindsight = Data + wisdom + perspective - Julia Hartz #femalefounders

- Think abt who,why,when,what as you grow a company and figure out who should be in leadership roles - Julia Hartz #FemaleFounders

- Julia Hartz: when a company is growing one of the biggest ways to blow it is to put the wrong person in a leadership role #FemaleFounders

- Retweeted by Shuba S.Inspiring that some one is starting early, reminds me of taking my daughter to business meeting #femalefounders pic.twitter.com/AcLTeEoSXq

- Adora is awesome, really funny. Needed to learn to be a good house cleaner, first idea was to read some how-to books :) #femalefounders

- 34.5% of female founders co-found with a spouse/SO! wow! #femalefounders

- Retweeted by Shuba S.#femalefounders is all women. Feel like what a guy would feel like at a normal tech conference.

- Specifically for women: it's possible to combine startups and kids, but easier without kids. But it can be done. #femalefounders

- Jessica's advice - need determination, withstand rejection, empathy, make something ppl want, live cheap, and FOCUS #femalefounders

- Jessica is on stage describing how YC started #femalefounders

Matisse Yoshihara

Matisse Yoshihara  Edith Yeung

Edith Yeung

Shuba S.

Shuba S.  treadfast

treadfast  Rebecca Goberstein

Rebecca Goberstein

WomenInnovateMobile

WomenInnovateMobile  EricaJoy

EricaJoy  rachelsklar

rachelsklar  Tracy Lawrence

Tracy Lawrence

Helena Powell

Helena Powell

cubitplanning

cubitplanning  Tracy Chou

Tracy Chou  Nidhi Aggarwal

Nidhi Aggarwal

Alexia Tsotsis

Alexia Tsotsis